No-Code Automation in Financial Services: Why Banks Can’t Afford to Wait

|

Getting your Trinity Audio player ready...

|

Here’s something most bank executives won’t admit publicly: they’re terrified of being left behind.

And honestly? They should be.

While traditional banks spend 18 months building a loan application feature, fintech startups are launching entire products in weeks. The gap isn’t talent or capital—it’s approach. No-code automation in financial services has quietly become the secret weapon that’s leveling the playing field.

I recently spoke with a CTO at a mid-sized credit union who told me they cut their loan approval time from two weeks to under two days. The kicker? They didn’t hire a single developer. Their compliance team built the whole thing themselves using a no-code platform.

That’s not an outlier anymore. It’s becoming the norm.

What Is No-Code Automation in Banking?

Let’s cut through the jargon. No-code automation means building workflows and applications without writing code. Instead of developers typing commands, business users drag and drop visual elements to create what they need.

Think of it like this: traditional coding is like writing a novel in a foreign language. No-code is like filling out a really smart form that builds the novel for you.

Your loan officer can create an approval workflow. Your compliance person can build a KYC check system. Your operations manager can automate monthly reports. All without bothering IT.

The technology handles surprisingly complex stuff too. We’re talking multi-step approvals, integrations with your core banking system, real-time data syncing across departments—things that used to require six-month development projects.

How Banks Actually Use This Stuff

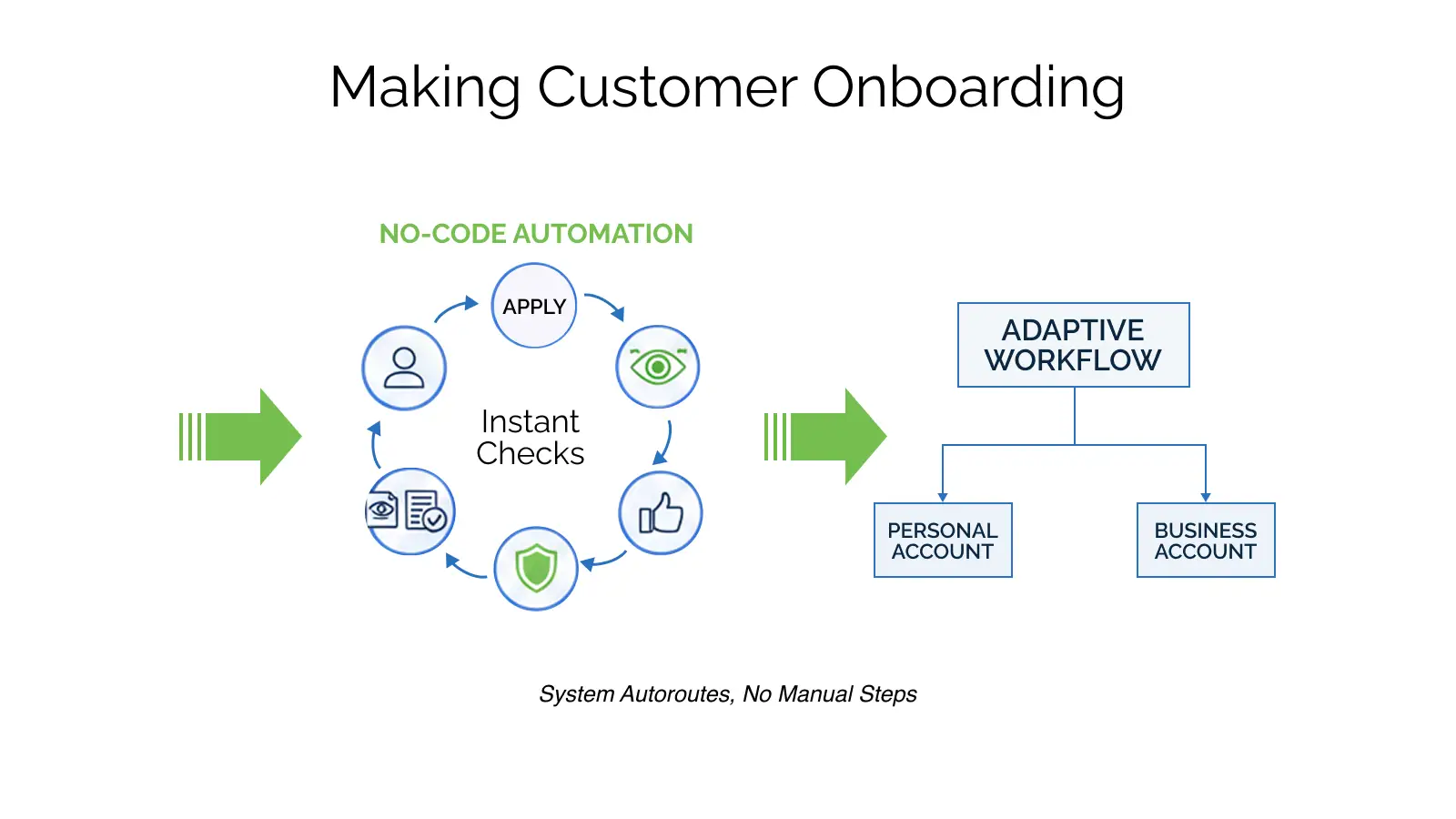

Making Customer Onboarding Not Suck

You know what kills customer acquisition? Slow onboarding. People apply for accounts and then… wait. And wait. Meanwhile, they’re getting approved at your competitor in 20 minutes.

Banks using no-code automation for lending are compressing what used to take days into same-day approvals. The system runs identity checks, pulls credit reports, validates information, and sets up accounts—all automatically.

Here’s what’s clever: it adjusts based on who’s applying. A business account follows different steps than a personal one. High-value customers trigger enhanced verification. The system figures out the right path without someone manually routing each application.

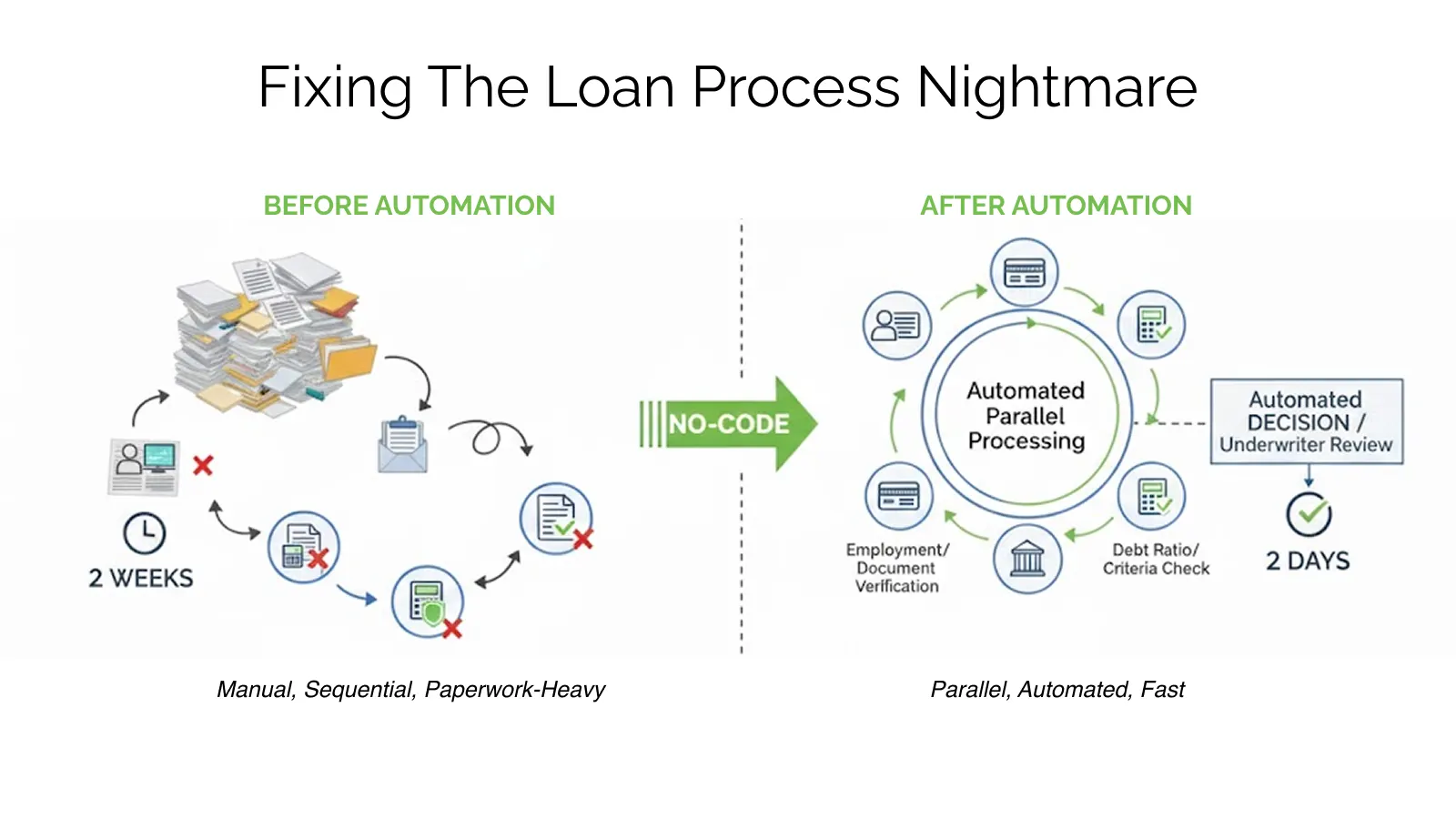

Fixing the Loan Process Nightmare

Let’s be honest—the traditional loan process is brutal. Papers everywhere, constant back-and-forth, applications sitting in limbo while different departments do their thing.

No-code automation in lending changes the game. When someone submits an application, the system automatically pulls their credit, calculates their debt ratios, checks them against your lending criteria, and sends everything to the right underwriter.

But here’s where it gets interesting: everything happens in parallel instead of sequentially. While the credit check runs, the system is also verifying employment, requesting documents, and checking collateral. What used to take two weeks now takes two days.

One regional bank told me they’ve automated about 40% of their loan decisions completely. The straightforward applications—good credit, sufficient income, reasonable loan-to-value—just approve automatically. Their underwriters now spend time on the complex cases that actually need human judgment.

Back-Office Operations That Don’t Require Overtime

Back-office work in banks is mind-numbing. The same processes, over and over. Reconciliations, exception handling, report generation. It’s all necessary, none of it is exciting, and it eats up massive amounts of time.

Banking workflow automation tackles this head-on. When transactions fail validation, the system automatically categorizes the issue, assigns it to the right person, escalates if it’s not fixed fast enough, and documents everything for compliance.

Account reconciliation—comparing your records against external statements—happens automatically now. The system only flags genuine problems for human review. Everything else? Handled.

I talked to an operations manager who said their month-end closing process used to require people working weekends. Now it runs automatically overnight. The team comes in Monday morning to review reports, not generate them.

Why Credit Processing Needed This Yesterday

Credit decisions are tricky. You need speed (customers want answers now) and accuracy (bad loans sink banks). No-code automation for credit processing delivers both.

The system encodes your lending policies into workflows. A personal loan under $10k for someone with a 750 credit score and stable employment? Auto-approved. Applications that fall into gray areas go to underwriters with all the relevant information already pulled and organized.

What I love about this: when things change, business users update the rules themselves. Market shifts, regulators issue new guidance, your risk appetite changes—you modify the workflow in an afternoon, not in six months of development sprints.

This flexibility matters enormously for specialized lending. Equipment financing works differently than commercial real estate, which works differently than small business loans. You can build tailored workflows for each without multiplying your IT headcount.

Digital Transformation That Actually Means Something

Everyone talks about digital transformation in financial services. Most of it is buzzword bingo. Real digital transformation means fundamentally changing how work happens.

Legacy banks operate in silos. Retail doesn’t talk to commercial. Lending doesn’t talk to wealth management. Nobody shares information, so customers get treated like strangers every time they interact with a different department.

No-code platforms break this down. A mortgage application can automatically trigger insurance product offers from another department. A business line of credit might surface merchant services opportunities. These connections happen naturally when systems can actually talk to each other.

Plus, the speed of change is different. Want to test a new loan product? Build a pilot workflow in days. Results disappointing? Change course without having wasted months of development.

This changes culture. Teams become willing to experiment because failure becomes cheap. That’s when innovation actually happens.

Where This Makes the Biggest Difference

AMLActually Implementing This Compliance (The Necessary Evil)

AML compliance is mandatory, expensive, and constantly evolving. Nobody loves it, everyone needs it.

AML compliance automation monitors transactions against watchlists, flags suspicious patterns, generates SARs when needed, and keeps detailed records. When regulators update watchlists or change screening rules, the system updates automatically.

Your compliance team focuses on investigating actual suspicious activity instead of configuring monitoring systems. That’s a better use of expensive expertise.

Catching Fraud Before It Costs You

Fraud detection automation analyzes transactions in real-time. Unusual amounts, geographic weirdness, velocity concerns—the system spots patterns and either blocks transactions, requests verification, or alerts your fraud team.

The smart implementations combine machine learning with business rules. Algorithms catch subtle patterns, business rules enforce obvious red flags. When fraud techniques evolve (and they always do), analysts adjust detection parameters immediately instead of waiting for IT to update code.

Loan Origination Without the Chaos

Modern loan origination involves dozens of steps: application, credit check, income verification, appraisal, title search, insurance, underwriting, pricing, disclosures, closing docs. Each step involves different people and often external vendors.

No-code automation for loan processing coordinates all this chaos. The system enforces timelines, sends reminders, provides status updates to borrowers and loan officers, and makes sure nothing falls through cracks.

A mortgage broker told me their loan officers used to spend half their time tracking down status updates. Now they spend that time with customers instead. That’s the kind of change that affects revenue, not just costs.

Risk Management That Doesn’t Rely on Spreadsheets

Risk management automation pulls data from trading systems, loan books, and investment accounts to calculate exposures, concentration limits, and capital requirements.

When limits get breached, the right people get notified immediately with context-rich reports. Risk managers shift from gathering data to actually analyzing it. Seems obvious, but plenty of banks still have senior people building Excel reports.

The No-Code vs. Low-Code Debate Nobody Asked For

People love arguing about no-code vs low-code in financial services. Here’s the actual difference that matters:

No-code: zero programming knowledge required. Business users build everything through visual interfaces. Limitations exist for super custom stuff.

Low-code: visual development with the option to add code when needed. More powerful, requires technical skills.

For banks, it’s not either/or. Use no-code for business-led automation—workflows, reports, data collection. Use low-code when you need extensive customization, like customer-facing apps.

The real question isn’t which is better. It’s which solves your specific problem. Automating loan approvals? No-code works fine. Building a next-gen mobile banking app? You’ll probably need low-code.

The Security Question Everyone Asks

Is No-Code Automation Safe for Banks?

This always comes up. Banks handle sensitive data under strict regulations. Trusting business users to build workflows sounds risky.

Modern enterprise platforms address this through layers of security:

Data gets encrypted at rest and in transit using AES-256—the same standard required for customer financial data.

Access controls enforce role-based permissions. People only see and do what their job requires. Multi-factor authentication adds another layer.

Audit logs track everything. Who built what, who approved which workflow, who accessed which data, when. These logs satisfy regulatory requirements and support investigations if something goes wrong.

The right platforms have SOC 2, ISO 27001, GDPR compliance. Many get PCI-DSS certification for payment processing.

The security question isn’t really about the technology. It’s about governance. Who can build workflows? What approval process applies before production deployment? What testing happens beforehand?

Answer those questions properly and no-code platforms are as secure as anything else in your environment. Ignore them and you’ll have problems regardless of your technology choices.

What You Can Actually Automate

Almost anything repetitive and rule-based qualifies. Here’s what banks are automating today:

Customer stuff: Account opening, loan applications, service requests, complaints, document collection, appointment scheduling.

Back-office: Transaction processing, reconciliation, exception handling, reports, regulatory filing, inter-department handoffs.

Compliance: KYC verification, sanctions screening, transaction monitoring, audit trails, risk scoring, regulatory reports.

Internal operations: Employee onboarding, access provisioning, expense processing, procurement approvals, training enrollment.

The common thread? These processes follow predictable patterns with clear decision points. They consume staff time without requiring deep expertise for most steps.

What you can’t automate: judgment calls, relationship management, complex negotiations, creative problem-solving. Basically, the stuff that actually requires humans.

The Economics Actually Make Sense

Traditional software development in finance costs a fortune and takes forever. Business requirements get translated to IT, developers build stuff, testing happens, deployment occurs, maintenance begins. This takes months or years and costs hundreds of thousands to millions.

A custom loan origination system built traditionally might need six developers for eight months at $150k per developer annually. That’s $600k in labor before you add project management, infrastructure, and testing. Total cost easily exceeds $1 million.

The same system on a no-code platform? Maybe two business analysts for three months, plus one technical architect for integrations. Total cost under $100k.

Maintenance costs diverge even more. Traditional systems need developers for every change. Updating a credit policy might take weeks of development and testing. The same change in a no-code workflow takes minutes.

Plus, traditional systems become technical debt. Original developers leave, documentation disappears, and modifying anything becomes scary and expensive. No-code platforms essentially document themselves through their visual nature.

Picking the Right Platform

Not all no-code platforms for banks work for regulated institutions. Consumer tools like Airtable or Zapier lack the security, compliance, and scalability you need.

Enterprise platforms designed for banking offer specific things:

Integration with core systems is non-negotiable. The platform must connect with your existing infrastructure—core deposits, loan servicing, general ledger, CRM, document management. Pre-built connectors make this easier.

Compliance features should be built-in, not bolted on. Look for approval workflows, version control, rollback capabilities, comprehensive audit logs.

Scalability matters as you expand. Can it handle thousands of concurrent workflows? Does performance degrade with complexity? What’s the uptime record?

Governance controls prevent chaos while enabling innovation. Admins need visibility into all workflows, the ability to enforce standards, and control over production deployment.

Financial services expertise separates generic platforms from banking-focused ones. Does the vendor understand your regulatory constraints? Can they reference similar implementations? Do they offer compliance documentation?

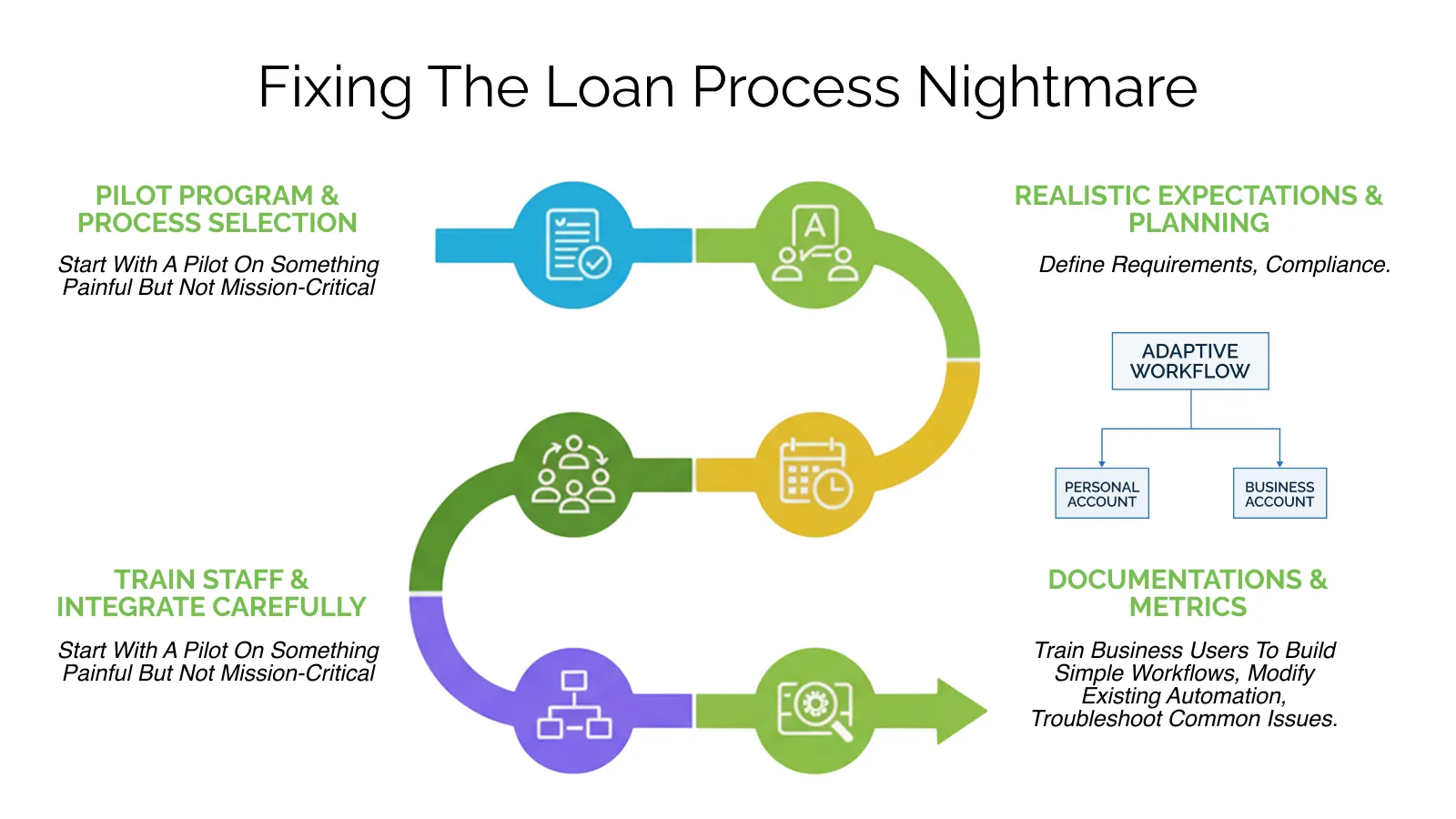

Actually Implementing This

Rolling out banking process automation tools requires more than buying software. It’s organizational change.

Start with a pilot on something painful but not mission-critical. Loan processing exception handling works great—it’s frustrating, time-consuming, and fixing it won’t bring down the bank if something goes wrong.

Build cross-functional teams. Include business users who know the process, compliance people who ensure regulatory compliance, IT folks who handle integration and security. Pure IT-led initiatives usually fail because business context gets lost.

Set realistic expectations. No-code is faster than traditional development, but proper implementation still needs requirements gathering, workflow design, testing, and training. Plan for 6-8 weeks on a pilot.

Document everything. Map current vs. future state, identify integration points, establish success metrics. This serves both as implementation guidance and compliance evidence.

Train extensively. The power of no-code is wasted if only IT uses it. Train business users to build simple workflows, modify existing automation, troubleshoot common issues. This creates a culture of continuous improvement.

Common Ways This Goes Wrong

Organizations rushing into no-code often hit predictable problems.

Automating broken processes is the biggest mistake. If your loan approval is slow because it has twelve unnecessary steps, automating those twelve steps makes a bad process fast, not good. Fix the process first.

Insufficient governance creates chaos. Different departments build incompatible solutions using different platforms. Establish governance early—not to slow things down, but to ensure innovation scales sustainably.

Neglecting change management kills even technically successful projects. Staff who fear automation will resist it. Involve them in design, address concerns directly, show how automation eliminates frustration rather than jobs.

Over-customization defeats the purpose. Platforms offer templates and best practices for good reasons—they reflect proven approaches. Customize thoughtfully, not reflexively.

Ignoring integration complexity creates data silos. Workflows that can’t access core systems or share data across departments deliver limited value.

Measuring What Actually Matters

Implementing automation without measuring results wastes money. Track these things:

Cycle time reduction: How much faster do processes complete? Loan approval dropping from seven days to three days is a 57% improvement.

Error rate reduction: Manual data entry errors requiring correction dropping from 12% to 2% saves money and frustration.

Cost per transaction: If processing a loan application cost $150 in staff time and now costs $60, that’s $90 saved per application.

Customer satisfaction: Faster processing, fewer errors, better communication all influence how customers perceive you.

Staff capacity freed: If automation eliminates 20 hours per week of manual work, what valuable activities can that person now pursue?

These metrics tell different stories to different audiences. Executives care about costs and competitive positioning. Department heads care about capacity and satisfaction. Regulators care about error rates and compliance.

Building Internal Capability

The term “citizen developer” describes business users who build applications. Developing these people transforms no-code from a tool into a capability.

Start by identifying natural candidates—process-oriented thinkers who understand both business needs and systems. Often they’re already maintaining complex spreadsheets or documenting workflows.

Provide structured training from basic to advanced. Start with simple linear workflows. Move to conditional logic, integrations, data transformations. Advance to complex multi-step processes and exception handling.

Training alone doesn’t work though. People need time allocated for automation projects. Someone spending 2% of their time on automation won’t accomplish much. Dedicate 20-30% of certain roles to automation development.

Create communities where citizen developers share techniques, troubleshoot problems, celebrate wins. This accelerates learning and prevents duplicate effort.

Recognize automation success publicly. When someone automates a painful process, acknowledge it. Consider automation contribution in performance reviews. This signals organizational commitment.

Working with Outside Help

Many institutions lack internal expertise for enterprise automation. Partnering with agencies that specialize in no-code for financial services accelerates things and reduces risk.

Good agencies bring:

Cross-implementation experience: They’ve solved problems you’re facing for the first time. They know what works in regulated environments and what creates compliance headaches.

Deep platform expertise: They understand advanced features, best practices, workarounds that generalists might miss.

Regulatory knowledge: Agencies working exclusively with banks understand BSA/AML, GLBA, FCRA, and other relevant regulations.

Structure partnerships properly though:

Prioritize knowledge transfer over pure implementation. Your goal is building internal capability, not dependency on consultants.

Maintain joint teams where internal staff work alongside consultants. This ensures knowledge transfers.

Establish clear exit criteria before starting. What does “done” look like? When can your team maintain things independently?

What Happens Next

Understanding this matters less than acting. Here’s what to do:

This week: Identify three painful, repetitive processes. Ask frontline staff what frustrates them daily. Document one process in detail.

This month: Evaluate three enterprise no-code platforms. Most offer trials or pilots. Run a small proof-of-concept automating your documented process.

This quarter: Launch a formal pilot with executive sponsorship. Select 2-3 processes for automation. Build cross-functional teams. Set measurable success criteria.

This year: Scale what works. Train citizen developers. Establish governance. Build an automation roadmap. Measure ROI and adjust.

The institutions that thrive won’t have the best technology—they’ll leverage technology most effectively. No-code automation in financial services provides that leverage.

The question isn’t whether to automate. It’s whether to lead or follow. The gap is widening every month.

What are you going to do about it?

Need help getting started?

We work with banks and financial institutions to implement automation that delivers results while maintaining compliance. Let’s talk about your specific challenges and how automation can help. The sooner you start, the bigger your advantage.

Sandeep Kaur

No-Code low-Code Expert

Related Insights on Low-Code & No-Code Automation

Explore more expert articles, practical strategies, and real-world use cases to help you automate your business and build smarter workflows.

Frequently Asked Questions About No-Code Automation in Financial Services

What is no-code automation in financial services?

It’s a way to build workflows and apps without actually coding. You drag and drop visual elements instead of writing lines of code. Your business team can create what they need without waiting for developers.

How do banks use no-code automation?

Pretty much anywhere there’s repetitive work—loan processing, customer onboarding, KYC checks, fraud detection, compliance reports, account reconciliation. If it follows a predictable pattern and eats up time, banks are automating it.

Is no-code automation safe for banks and financial institutions?

When you use enterprise platforms built for regulated industries, yes. These aren’t consumer tools—they come with bank-grade encryption, proper access controls, audit logs, and certifications like SOC 2 and ISO 27001. The security is there if you choose the right platform.

Is no-code automation compliant with financial regulations?

Compliance isn’t automatic—it depends on how you implement it. Good platforms give you the tools: audit trails, version control, approval workflows. But you still need to work with your compliance team to make sure everything meets regulatory requirements.

What banking processes can be automated using no-code platforms?

Account opening, loan applications, reconciliation, exception handling, reports, KYC verification, AML screening, risk assessments, employee onboarding, approval workflows—basically anything repetitive that doesn’t need human judgment for every single step.

How does no-code automation improve loan approval and credit processing?

It runs everything in parallel instead of one thing at a time. Credit checks, income verification, and risk assessments all happen simultaneously. Simple applications get auto-approved, complex ones go to underwriters with everything already organized. What took two weeks now takes two days.

What is the difference between no-code and low-code in financial services?

No-code is purely visual—no programming needed at all. Low-code lets you add custom code when you need extra functionality. Most banks use no-code for internal workflows and low-code when they’re building customer-facing apps that need heavy customization.

Can no-code platforms integrate with core banking systems?

Yes, though it depends on the platform. Enterprise-grade ones come with APIs and pre-built connectors for core banking systems, loan servicing platforms, CRMs, and document management. Integration capability is actually one of the main things to check before choosing a platform.